- Structures to Support Business Activities

-

- Corporate Governance

- Sumitomo's Business Philosophy / Sumitomo Corporation Group's Corporate Mission Statement

- Corporate Governance System

- Internal Control and Internal Audits

- Compliance

- Risk Management

- Human Resource Management

- Towards a Better, Sustainable Society (CSR)

- Message from the Chair of the CSR Committee

- Environmental Initiatives

- Social Initiatives

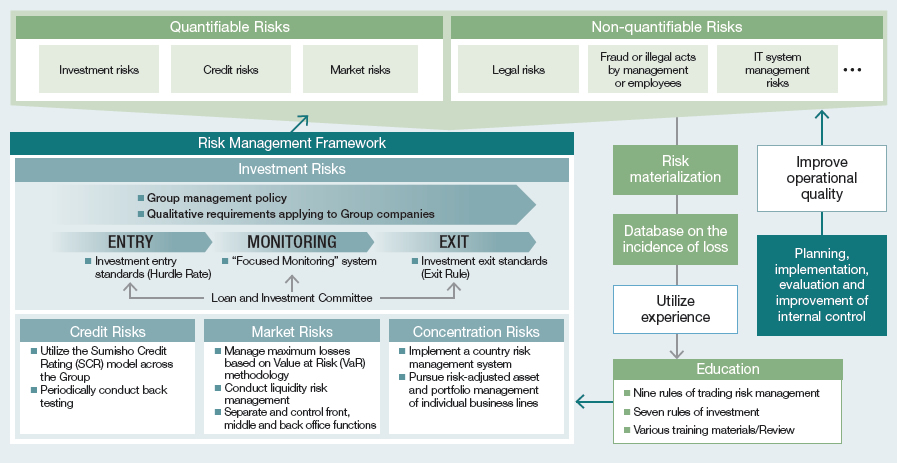

Risk Management

In order to cope effectively with the diversifying risk environment, we have built a risk management framework by developing our risk management approach from a micro to a macro perspective, and shifting our focus from "minimizing losses from individual transactions" to "maximizing corporate value." This framework is strongly linked to the management plan, playing a critical role in supporting the efficient management of our corporate resources.

The Purpose of Risk Management

We define "risk" as the "possibility of losses due to the occurrence of anticipated or unanticipated situations" and as the "possibility of not achieving the expected return on business activities." We have set the following three items as the purpose for our risk management activities.

- Stabilize Performance: Minimize discrepancies between the plan and the actual results

- Strengthen Financial Base: Maintain Risk-adjusted Assets within the buffer (shareholders' equity)

- Maintain Corporate Reputation: Fulfill CSR requirements and preserve corporate reputation

Risk Management Basic Policy

We classify our risks into two categories: Quantifiable risk and Non-quantifiable risk. Quantifiable risk is defined as "value creating risk," which we proactively take to generate a return. Our policy is to maximize the risk-adjusted return while maintaining Risk-adjusted Assets within our buffer.

Non-quantifiable risk is defined as "value breaking risk," which only generates losses when it surfaces. We are building a framework that prevents or minimizes the probability of this risk from materializing.

Risk Management Framework

Managing Quantifiable Risk

Managing Investment Risk

Once an investment is made, it is often difficult to make a withdrawal decision and the loss impact is usually significant in scale. To manage the investment risk, we have in place an integrated framework covering the entry process to the exit process. For the entry process, we carefully select investments that exceed the hurdle rate, a threshold for the rates of return on new investments based on the cost of capital. In case of new large-scale investments or projects, cases are submitted to the Loan and Investment Committee for thorough examination. The Committee is also responsible for monitoring the preparation and implementation of necessary measures to improve the performance of the existing important investments. When the performance of investments falls short of required standards after a certain period from its inception, we have an Exit Rule that designates such investment as "Investment to withdraw from."

Managing Credit Risks

Our business is exposed to credit risks, as we extend credit to our customers in the form of accounts receivable, advances, loans, guarantees and other instruments. We have incorporated our original credit rating model, the Sumisho Credit Rating (SCR), to assess our customers' credit risk. The authority level to provide credit exposure to customers depends on the assigned credit rating. In addition, we regularly review customers' credit limits and appropriately manage the credit exposure under those limits. At the same time, we continuously perform credit evaluations on the financial condition of customers, and based on such evaluations, take collateral to secure the receivables if necessary.

Managing Market Risks

We set limits on contract balances as well as the loss limits for six months for commodity and financial instrument transactions. At the same time, we constantly monitor the potential amount of loss, (Value at Risk (VaR)—an estimate of potential risk or in case the total figures of realized and unrealized gain/loss are negative at the time of monitoring, the total of VaR and the relevant negative figures), to ensure that the potential amount of loss falls within the loss limits. In addition, we conduct liquidity risk management for each product on an individual futures market basis in order to be prepared in the event that it becomes difficult to close positions due to shrinking liquidity. The Financial Resources Management Group undertakes both the back and middle office functions in order to completely separate those functions from the Business Units, thereby enabling us to maintain the soundness of internal checks.

Managing Concentration Risks

As we are operating globally and engaging in a variety of business fields, we need to ensure that the risks are not excessively concentrated in particular areas. In order to avoid overly concentrated exposure in certain countries and regions, we have in place a country risk management system. In addition, in order to avoid the excessive concentration of resources in any specific field and refine our business portfolio, we thoroughly discuss the amount of Risk-adjusted Assets distributed to each unit and business line in meetings such as the "strategy conference," which is held among the President and CEO and general managers of each unit and the "Loan and Investment Committee," which deliberates on important investment and financing.

Managing Non-quantifiable Risks

Non-quantifiable risks are those that must be borne, but for which we cannot expect returns. These include litigation and other legal risks, operational risks such as clerical mistakes or fraud acts, and natural disaster risk. Some of these risks involve events that rarely occur but could have a critical impact on our operations once they arise. Our basic policy is to prevent or minimize the probability of these risks to materialize. Accordingly, we periodically assess non-quantifiable risks on a global and consolidated basis. We do this through a range of initiatives to strengthen our internal control across the Group under the leadership of the Internal Control Committee as well as through independent activities by our Business Units and regional organizations in Japan and overseas. Based on the assessment result, we continuously search for a more efficient and effective organizational structure and procedures to improve the quality of our business operations.

Embedding the Sense of Risk Management

Although we have been constructing the best possible risk management framework to cope with diversified risks, we cannot completely prevent the incurrence of loss in the course of business activities only by the framework itself. We are putting our efforts into implementing the initiatives that enable us to quickly identify the occurrence of losses in order to suppress loss accumulation and prevent the contagion effects that lead to secondary losses. These initiatives include devising ways to quickly identify the cause of losses and share such information among top management and related departments. We have compiled a database of such loss information that allows for the systematic analysis of the causes of loss-incurring events. These analyses are used as training materials for employees as part of various educational programs. Through this knowledge feedback process, individual employees can upgrade their risk management capabilities, supporting the prevention of the same kind of loss events.

Eyeing the Future of Risk Management

Sumitomo Corporation has created a formidable risk management framework by studying advanced methods and processes. Our goal is to implement the best practices in risk management while maintaining the flexibility to adapt to changes in the business environment. The surrounding environment is continually changing, however, and new business models that we could never have imagined are emerging on a daily basis. Responding to changing circumstances in a timely and effective manner, we continually upgrade our risk management under the direction of top management.

Information Security Control Structure

Sumitomo Corporation works to enhance its information management system to maintain and improve information security. Our approach to this end includes the development of internal rules and manuals as well as the provision of employee training and awareness-raising activities, with a focus on taking preventive measures against risks relating to leakages of confidential information and compliance with the Personal Information Protection Act, which came into full effect in April 2005.

Risk-adjusted Return Management

We are now facing a harsher business environment compared to the past few years, during which we saw steady growth. However, we have been implementing management reforms on the basis of the Risk-adjusted Return Approach for many years, building a business foundation able to sustain stable earnings and a firm financial condition even during severe economic environments. In this special feature, we will introduce Risk-adjusted Return as the backbone of our management approach.

Background to the Introduction of the Risk-adjusted Return Ratio

Until the early 1980s, the main business of Sumitomo Corporation and other integrated trading companies was acting as intermediaries for goods and services. From the late 1980s onward, integrated trading companies sharply stepped up their involvement in new businesses as well as overseas investment as they responded to a decline in demand for trading company financing and the growing transfer of production overseas due to the yen's appreciation.

In the early 1990s, in addition to this business diversification, a series of changes came about in the operating environment. The collapse of the bubble economy in the early 1990s triggered a plunge in stock and real estate prices, and in 1997, the Asian Currency Crisis caused problems for many overseas projects. In addition to the effects of these factors, we recorded substantial impairment of shareholders' equity due to an incident involving unauthorized copper trading in 1996. Thereafter, improving profitability and our financial condition became our topmost priority.

As our Business Units have a variety of business styles in diverse fields, it was difficult to evaluate each business's performance based only on profit for the year. We needed a Company-wide, universal yardstick for measuring the return on management resources invested in each business and for optimally allocating limited management resources.

The basic aim of any business is to generate returns relative to the risks involved and in autumn 1998, ahead of its peers, Sumitomo Corporation introduced the Risk-adjusted Return Ratio as an indicator of profitability, i.e., the degree of return from a certain level of risk.

Specifically, we calculate Risk-adjusted Assets as the value of maximum possible losses by multiplying the value of assets by a risk weight that assumes the maximum possible loss ratio in asset values.

With Risk-adjusted Assets as the denominator, we use returns, i.e., profit for the year, as the numerator to calculate profitability, both in each business and for the Company as a whole.

Basics of Risk-adjusted Return Management

Since its introduction as a management indicator, the Risk-adjusted Return Ratio has played a major role as a tool for achieving universal Company-wide objectives.

From the perspective of ensuring business stability, a core management principle is to avoid excessive risks by keeping Risk-adjusted Assets (maximum possible losses) within shareholders' equity (the risk buffer). This principle means that even if all potential risks were to actually occur at once, shareholders' equity would be able to absorb the losses.

Moreover, to ensure earnings power, return on risks must be greater than our shareholders' capital cost. In other words, we set the Risk-adjusted Return Ratio at 7.5% as the minimum requirement for the whole company. In every business, the basis we use for choosing to move forward is this Risk-adjusted Return Ratio of 7.5%.